The fintech segment is expected to experience significant growth, with revenues projected to range from $245 billion to $1.5 trillion by 2030.

Apps became platforms. And then platforms became ecosystems. Loans. Payments. Wealth management. Insurance. Compliance. Embedded finance. Fintech is involved everywhere. Users have come to demand it. They have come to depend on it. Apps are no longer “nice to have.” They are “need to have.”

Fintech app development, or any other type of software development, is more than just coding.

This article examines the essential trends related to the evolution of the fintech industry and how companies and software developers can create innovative and secure apps and make them scalable and competitive.

Understanding the Fintech Landscape Today

Fin-tech is where finance, technology, and regulatory laws converge. Fin-tech apps are different from other apps because these apps deal with personal information, actual money, and “legal obligations.” It offers immense opportunities, along with immense complexity.

Today’s users want the ability to access everything immediately. Real-time payments. Real-time balance updates. Customized analytics. Seamless onboarding. Today’s users want mobile apps to be fast, smart, and easy to use. However, the government wants users to be compliant, transparent, and protected.

The need for balance between speed and safety is paramount. The need for convenience and control to coexist is paramount. The need for UX and security to coexist is paramount. Effective apps address competing requirements through proper design and infrastructure.

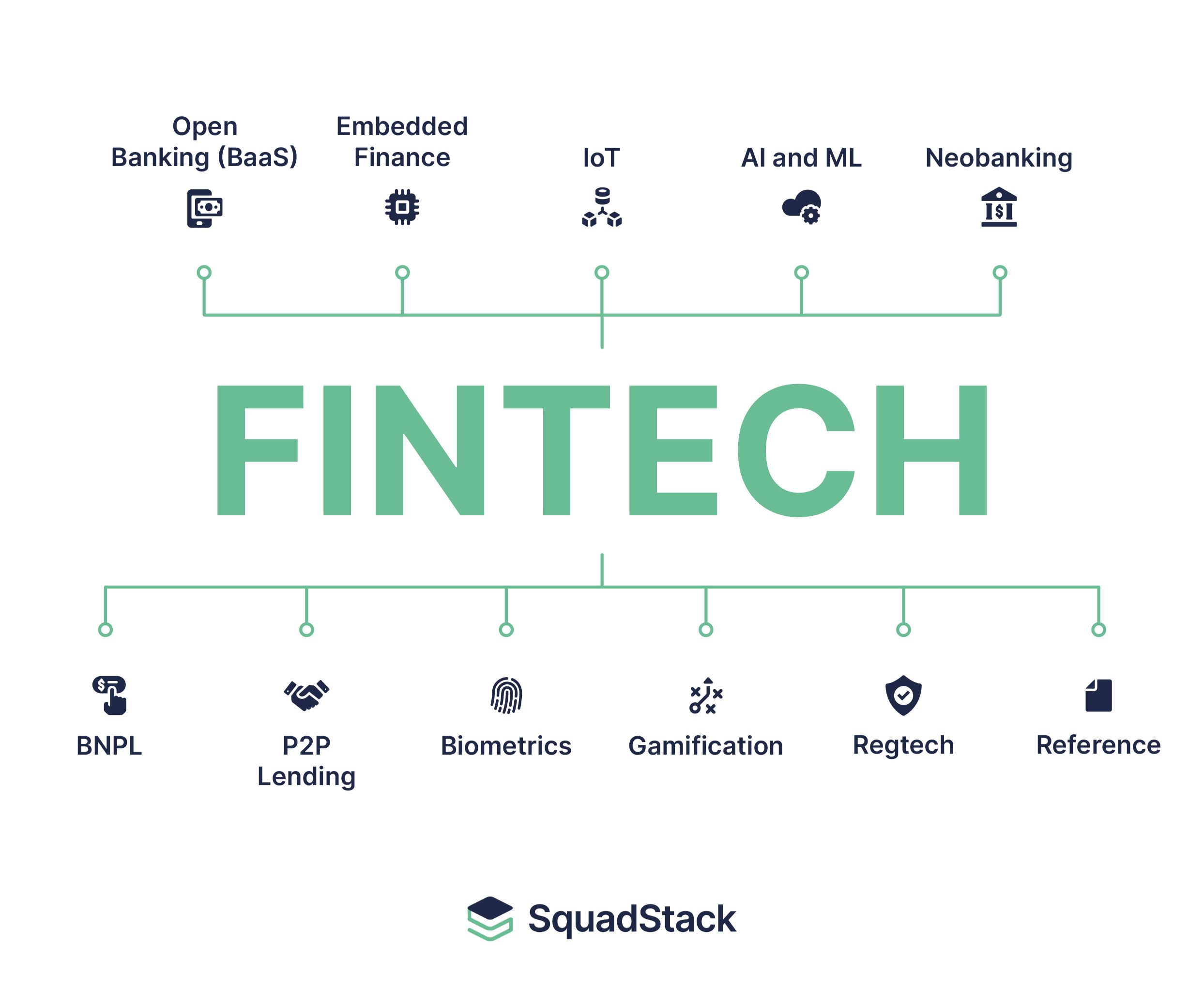

There is a wide range in the fintech industry. Digital banks. Payment gateways. Lending apps. Investment solutions. Insuretech. Infrastructure companies. Each domain comes with its own set of challenges. However, similar trends also apply. These need to be understood. They can render apps outdated.

Digital Banking and Neobanks

One of the most popular fintech trends is the digital-only bank. Neobanks are banks that function solely from mobile applications. No need for branches, paperwork, and long lines. They rely heavily on UX and minimal fees. Opening an account takes minutes, and notifications come almost instantly.

For app developers, this means apps must be fast, trusted, and stable. Basic banking operations must never fail. Unavailability of services leads to loss of trust right away.

Main areas of focus: secure authentication, transaction handling, and government regulations. Innovations are stacked on top: budgeting, automated savings, and expense analysis. Foundation first. Features next. Performance is first and foremost.

Users want more than the bare essentials. This is where smart insights and smart guidance come in. Apps need to be more personalized than intrusive. This is the norm now.

Embedded Finance and APIs

The finance-embedded model is revolutionizing the way people receive services. There are no longer any banking applications required to access finance services. Banking functionality is embedded within other applications. Online markets now offer loans when purchasing products. SaaS applications embed payment functionality. Ride share applications include wallets and immediate payments.

APIs make it seamless. Modular infrastructure connects everything. Applications need to be API first. Integration needs to be secure, efficient, and invisible. Payment processing, identity verification solutions, and compliance software can work in concert in the background. Users experience simplicity; complexity gets hidden.

“It is a design revolution that stresses user-centered design.” Banking and financial engagement must become seamless extensions of the original product. Professional mobile app development services simplify complexity in banking apps and help consumers see through the noise, making them truly unique.

Real-Time Payments and Faster Settlement

Speed is non-negotiable. Users expect money to be transferred instantly. They need instant confirmations. They need their account balances to be updated.

Real-time networks are spreading worldwide. Applications based on these have a competitive advantage. Its implementation needs event-driven design and monitoring. Accuracy cannot be compromised.

Innovation is not only speed. Transparency is important. Users want to know when, where, and why transactions occur. Transparency encourages trust. Users are less anxious. They have a sense of control.

Artificial Intelligence and Finance that Relies on Data

AI integration is becoming more integral to fintech services. Fraud analysis. Personalization, customer service, and AI predictive analysis. Applications offer the capability to predict expenditure, make savings suggestions, and evaluate creditworthiness.

Artificial intelligence requires proper governance. Data is considered to be sensitive. Artificial intelligence models have to be explainable, fair, and compliant. Black box artificial intelligence gives rise to challenges from a legal and ethical perspective.

But the role of the AI is only to empower the decision-making process, not replace the decision itself. Provide insights. Suggest smarter decisions. Hint at the next actions. When done properly, AI establishes trust. When done inadequately, it

Blockchain Technology and Decentralized Finance

Blockchain technology is still making waves in the fintech world. Payment systems. Money transfers. Portfolio management. DeFi is still quite volatile, although some solutions are very useful.

Cross-border payments are faster. Middlemen are reduced. Tokenization facilitates new investing patterns. Immutable books enhance certainty.

Users care about outcomes, not technologies. Wallets must be simple to use. Keys must be secure. Transactions should be evident. Complexity in blockchain should be invisible. Innovation often involves making something complex seem familiar.

Regulatory Technology and Compliance Automation

Compliance must always be adhered to strictly. The rules keep changing continuously. Data protection. AML.

Regtech can do the work automatically, like identity verification, transaction monitoring, and reporting. Risk is decreased with.

Integrating compliance is essential. It is very expensive when done through retrofitting. Apps with innovative designs use compliance as an enabler. There is clarity in onboarding. There is transparency in disclosure. There are automated tests. Users experience trust. Regulators have a

Security & Privacy by Design

Security is a priority. Customers place money and private information into apps. Trust is lost once.

There have to be multiple levels: encryption, tokenization, secure authentication, and monitoring. Privacy by design matters too. “Customers demand control.” Consent needs to be understandable. Privacy policies have to be transparent.

Security is not an option, but is architecture by definition. Audits, penetration testing, and incident response are all important features of that architecture.

User Experience and Accessibility / CSS Guidelines

Complexity is inevitable, but usability has to be simple. Users always need simplicity, speed, and clarity.

Good UX can decrease cognitive load. Information should be readable. Actions should be reversible. Accessibility is imperative. Users come with their devices, abilities, and financial literacy levels.

Innovation lies in the details of micro-interactions. Good visual hierarchies are essential. Simple language helps too.

Creating Scalable Fintech Architectures

Scalability is necessary. Unpredictable growth must be planned for. Scalable architectures assist with growth uncertainty in the cloud native world. Microservices.

Scaling is both technical and operational. Teams, processes, and culture must scale as well. CI/CD pipelines, automated testing, and monitoring become critical.

Data Integration and Financial Aggregation

Open banking facilitates account aggregation. It provides consumers with access to several accounts from one platform. Budgeting. Net worth. Investment.

Secure connection, consent, and data normalization are essential. Unfiltered data is meaningless. Information is valuable. Finances must be made understandable by apps. Successful apps make sense of finances.

Important Fintech Elements vs. User Expectations

| Feature | User Expectation | Risk of Poor Performance | In this context |

| Transfers | Fast and accurate | User frustration, lack of trust | Backend should be capable of handling real-time updates |

| Account Overview | Clear, readable dashboard | Trauma, frustration | Keep the images simple, the text concise |

| Notifications | Real-time, accurate | Fear, distrust | Provide explicit transaction information |

| AI Suggestions | Useful, personalized | Mistrust, experience of intrusion | Fairness, transparency, subtlety |

| Security | Strong, transparent | Breaches, reputation loss | Multi-layer encryption and tracking |

Monetization Models in Fintech Applications

Revenue has to be in balance with value. Subscriptions. Transaction costs. Interchange. Premium services. Hidden costs undermine trust.

Pricing affects behavior. Clear models promote loyalty. Monetization drives flows, functionality, and compliance.

Product Validation and Iterative Development

Apps succeed incrementally. MVPs test assumptions. Analytics and user research inform the product.

Releases are done after careful rollouts. Feature flags and sandboxes support controlled growth. Small improvements compound over time. Innovation is incremental.

Collaboration with Financial Institutions and Suppliers

Few applications succeed alone. Banks, processors, and infrastructure companies act as partners.

Choosing partners is critical. Reliable. Compliant. Scalable. With the right partners, focus remains on differentiation. Innovation builds on shared strengths.

Future Planning for Financial Technology

Fintech evolves daily. Regulations change. Technology advances. User expectations grow.

Apps have to be flexible. Adaptive. Strategic. Future apps will be proactive. Integrated into everyday life. Enabling and facilitating financial well-being.

Emerging Fintech Trends 2025

Trend | Description | Effect on Users | Implementation / Considerations |

| Embedded Finance | Finance is linked with other applications | Seamless experience, convenience | API-first, integration simplicity |

| Real-time Banking | Immediate payments and updates | Lower anxiety, increased trust | Event-driven backend, low-latency systems |

| Open Banking | Handling multiple accounts | Improved financial understanding | Secure consent flows, data access |

| AI Guidance | Personalized recommendations | Smart financial choices | Fair and transparent AI models |

| Blockchain Payments | Faster, cheaper transfers | Cost savings, trust | Hidden complexity, usability focus |

Conclusion

Fintech is a dynamic, highly competitive space filled with promise. Innovation is not about chasing trends but understanding users, regulation, and market reality. Link strategy to trends. Build secure, scalable, valuable apps. Honor trust. Embed compliance. Adapt continuously. The best fintech applications are innovative, thoughtful, and human. Made to last. Made to grow. Made to make finance simpler.